Behaviour change and infrastructure beyond Covid-19

Status:Final report complete.

Commission analysis of a range of scenarios for how the use of public transport, broadband networks and utilities might change as a result of the pandemic.

Executive summary

During the pandemic, a significant share of the population have been able to shift to radically different ways of working. New pressures have revealed the potential for long term changes in where people live and work and how they use infrastructure. However, the social, economic and physical connections that brought cities together before the pandemic are strong.

It is too early to assume that long term behaviour change will lead to wholly different patterns of infrastructure use. In the face of this uncertainty, long term infrastructure policy must consider the range of potential permanent changes in behaviour. This is increasingly important as policymakers begin to set out plans to deliver on the UK’s long term strategic infrastructure priorities.

Policymakers can plan for future infrastructure requirements by thinking about the realistic scenarios that could unfold, and how they could respond to the range of possibilities. This will help focus attention on the low regrets interventions that make sense across different scenarios, and on policies that can help decide the scenario by encouraging shifts in behaviour long term.

Making policy decisions during continued uncertainty may mean taking a more adaptive approach to longer term project commitments and investing in new data sources which can help understand how these changes are unfolding. All these approaches are preferable to planning on the basis of fixed assumptions about what will happen based on short term observations. The Commission’s analysis suggests that the spread of potential outcomes for transport, particularly public transport, is wider compared to digital, energy, waste and water.

Impacts of the Covid-19 pandemic on infrastructure

The Covid-19 pandemic and associated restrictions have had significant impacts on patterns of infrastructure use, particularly public transport. Following the announcement of the initial lockdown in March 2020, public transport use in the UK fell by 80 to 95 per cent for different modes and, as of April 2021, is still only seeing between 30 and 50 per cent of normal use.

Several pre-existing trends have been accelerated as a result of the pandemic, such as increases in the number of people working from home and the volume of ecommerce. Conversely, other historic patterns, such as trends in commuter travel, have been reversed, with significantly fewer people using rail to commute to work since the beginning of the pandemic.

As restrictions are eased, there is uncertainty about the extent to which these changes will revert or endure. Despite the extreme shift to homeworking at the beginning of the pandemic, one third of office workers in the UK returned to their normal place of work when restrictions were temporarily lifted in summer 2020, and across the rest of Europe, two thirds of office workers returned.

Understanding behaviour change

Some understanding of the scale of the potential long term impact on infrastructure of the Covid-19 pandemic can be developed using lessons from the theories of behaviour change and historic shocks.

Theories of behaviour change generally point to certain key conditions that make behaviour change more likely. These conditions include individual factors, such as personal motivation and capability, and external factors, such as the perceived or actual consequences of changed behaviour. This complex interaction of individual choices and external factors does not enable outcomes to be readily predicted.

Analysis of comparable historic shocks suggests that short term shifts in behaviour that occur after disruptive events don’t often indicate the long term outcome.

Previous experience of systemic shocks illustrates that they are more likely to cause long term changes if they trigger adaptation of routines or practices. Often, this is determined by the flexibility that individuals and firms have to adapt, how disruptive the shocks are and whether the impacts are prolonged. Not many previous shocks have had these features. For example, remote working in response to Hurricane Sandy in 2012 was only a temporary change as internet and business systems did not allow for productive working from home, which restricted the flexibility of individuals and firms to adapt, and the disruption did not persist for long enough to trigger long term change. In contrast, the current situation has lasted longer, and individuals and firms have had to find ways to adapt.

In some cases, policy interventions have influenced the impact and duration of shocks on infrastructure demand. For example, policies to educate the general population about the internet in South Korea alongside rollout of broadband during the first 20 years of this century – a technological ‘shock – catalysed behaviour change in recreation, social interactions and work and education activities.

Scenario analysis

No model can accurately predict how or whether the changes caused by Covid-19 will continue in the future. A more suitable approach is to consider different scenarios of how people’s behaviour might change and how policy can prepare and adapt accordingly.

The Commission has developed a set of scenarios that reflect different combinations of possible behavioural trends that could impact infrastructure use patterns. Quantitative analysis has been used to assess the implications that trends may have for infrastructure use and their magnitude.1

There are a wide range of possible outcomes for transport in particular. A rise in flexible working may result in permanently less commuting into offices – potentially affecting travel demand into bigger cities. People may seek to relocate from cities to more suburban and rural areas, if reduced need to commute means that people choose to live in quieter areas. This could affect travel patterns by causing people to commute less frequently but over longer distances or increasing car traffic in towns and suburbs. Transport may also be affected by a long term aversion to crowded spaces, causing people to avoid air travel or switch from public transport to cars. Travel for leisure may also face a decline if online shopping and entertainment remain permanently higher.

However, the long term attractiveness of flexible working to workers and employers remains unproven. The social and economic infrastructure that has drawn so many people to cities may continue to be attractive even if working patterns change. Similarly, if people wish to relocate, the availability of housing and other infrastructure in less densely developed areas may limit the extent to which this can happen in practice.

Quantitative analysis undertaken for the Commission suggests that the difference in average annual public transport trips between the scenarios with the highest and lowest levels of behaviour change could be as high as 25 per cent over the next 30 years. The variation in annual trips by car between scenarios is less but still marked, with a range of ten per cent between scenarios.

Even in scenarios where total change in demand is lower, the complexity of change in behavioural patterns may have material implications for infrastructure demand and decision making. Changes in the distribution of demand over time and place can be as significant as changes in its total level, particularly for networks that are built to manage peak time capacity. Flexible working may mean flatter peaks on public transport, potentially reducing the level of capacity required.

Additionally, modest changes in demand may also have disproportionate effects where crucial tipping points are reached. For example, a small amount of additional road traffic could lead to congestion in some town centres, potentially slowing journey times considerably. For some public transport services, a small reduction in passengers could lead to a downward spiral in revenues, possibly leading some services to be discontinued.

The implications for other sectors are likely to be less significant than for transport. The quantitative analysis suggests a ten per cent difference in digital demand in the next five years when comparing the highest and lowest behaviour change scenarios. However, this is unlikely to have a significant impact on network capacity given current trends of fast-growing demand.

The indicated variation in patterns of demand for utilities is even smaller. Scenarios for domestic use suggest a range of less than ten per cent compared against the highest scenario by the 2050s. However, the exact patterns of peak use will be important in both cases. Changes in patterns of demand that result in greater concentration at the busiest points in the day or week will pose greater challenges to service providers.

Preparing for the future

It is still far too early to draw conclusions about which behavioural trends may emerge in the long term as a result of the pandemic. In the UK, offices have not yet fully reopened. New arrangements are being proposed by several employers, but these are still to be tested. Social habits will not follow organisationally chosen pathways and may change direction some time after restrictions are eased.

However, the importance of a continued commitment to infrastructure remains high given its critical role in supporting policy goals, such as achieving net zero greenhouse gas emissions by 2050 and rebalancing economic growth across the UK. Although uncertainty may point towards delaying decisions on major infrastructure projects, there is also a case for the government to take decisions to reduce uncertainty and increase confidence for the market and for investors.

Alongside the role of infrastructure investment in the economic recovery, the government should maintain focus on future infrastructure needs to achieve long term goals. To inform upcoming decisions on infrastructure and remain responsive to a breadth of outcomes, policymakers should consider the following questions:

- What decisions are unaffected by uncertainty in behavioural patterns? Whilst outcomes for different sectors will vary depending on which scenario plays out, there are some areas which are likely to be less affected by the Covid-19 pandemic. For example, it is certain that in any scenario for behaviour change, decarbonisation of infrastructure will remain necessary to achieve net zero by 2050.

- When will it be clear which behaviours will be permanent? Better data gathering on indicators of how behaviour change may be manifesting, with attention to ensuring this data is timely, can help identify emerging behaviour change promptly. Additionally, it is important to avoid reliance on models that have not worked that well even under more stable conditions in the past.

- Should policy seek to influence which scenario unfolds? The outcomes of some scenarios are likely to be less preferable than others, with varying combinations of positive and negative consequences. Policymakers should consider how policy can encourage preferred shifts in behaviour. For example, as people’s patterns of transport use are changing in response to the pandemic, there is scope to encourage more active travel or avoid a recovery scenario in which travel by car rises relative to pre-pandemic usage. Transport providers can also consider how best to ensure consistent, evidence-based information is provided to give passengers confidence to use public transport.

- How can long term project commitments be reconciled with ongoing uncertainty? The portfolio of infrastructure investments can mitigate uncertainty by adopting a balance across different levels of risk, and having a complementary mix of programmes which cover different scenarios as well as low regrets options applicable across multiple scenarios. A particularly valuable tool may be an adaptive approach to investment, as considered by the Commission in the Rail Needs Assessment (RNA) for the North and Midlands. The RNA proposed moving forward with rail investment in stages as costs and benefits become clearer. An adaptive approach would allow for measured, forward momentum that can be modified as the long term behaviour changes become evident. In turn, this can help to preserve optionality and flexibility throughout a project. This will be particularly important in sectors where there is greater uncertainty, such as transport.

These considerations will guide the Commission in its future work, including making policy recommendations in the study underway on Infrastructure, Towns and Regeneration, and in the second National Infrastructure Assessment.

Next Section: 1. Impacts of Covid-19

The Covid-19 pandemic has had a significant impact on people’s daily lives by restricting them at home for extended periods, rapidly increasing adoption of homeworking and reducing the frequency of physical social engagement.

1. Impacts of Covid-19

The Covid-19 pandemic has had a significant impact on people’s daily lives by restricting them at home for extended periods, rapidly increasing adoption of homeworking and reducing the frequency of physical social engagement.

The pandemic has led to:

- a rapid uptake in working from home

- steep initial reductions in in-person social engagement levels, although these have recovered during times of reduced restrictions

- increased demand for rural housing and houses with better access to outdoor space

- a major reduction in public transport use, which has not fully recovered even during times of reduced restrictions

- a recovery in motor vehicle use, following an initial drop at the beginning of the pandemic, and an increase in commercial vehicle use

- increased rates of active travel, including cycling

- manageable increases in broadband data demand

- changes in patterns of demand for energy, water and waste, which have not had impacts on the relevant networks.

Any long term behaviour change due to Covid-19 is likely to be less radical than the changes seen during the peak of the pandemic. However, there is uncertainty about the long term impact of the pandemic and it is not yet possible to know which of the observed behaviours will endure.

Working from home

One of the pandemic’s key impacts has been a radical and rapid shift to working from home.2 Pre pandemic data shows that the proportion of people working mainly at home has been increasing over the past decades, reaching six per cent of workers in early 2020, with an additional quarter of all UK workers estimated to occasionally work from home.3

However, the pandemic has shown that a higher number of people can potentially work at home, with almost half of all UK employees doing at least some work at home in April 2020.4 In March 2021, one year after the introduction of social distancing measures, 30 per cent of employees were working from home exclusively and 12 per cent occasionally.5

Despite its widespread adoption, the opportunity to work from home has tended to be limited to certain types of occupations. Occupations requiring higher qualifications have been more likely to provide homeworking opportunities than elementary and manual ones.6 Table 1 presents a comparison of working patterns in April 2020 compared to 2019 for selected occupations that are more likely to adopt homeworking.

Table 1: Comparison of flexible and permanent homeworking patterns in 2019 (whole year average) and April 2020 for selected occupations, as a percentage of employees.

| Managers, directors and senior officials | Professional occupations | Administrative and secretarial cccupations | ||||

|---|---|---|---|---|---|---|

| 2019 | April 2020 | 2019 | April 202 | 2019 | April 2020 | |

| Not working from home | 75.7 | 43.6 | 79.7 | 38.3 | 89.5 | 50.7 |

| Working from home, of which | 24.3 | 56.4 | 20.3 | 61.7 | 10.5 | 49.3 |

| a) flexible | 14.3 | - | 14.5 | - | 3.7 | - |

| b) permanent | 10.0 | - | 5.8 | - | 6.9 | - |

A similar distinction between different occupations has also been prevalent across Europe, but overall full or partial homeworking adoption peaked at 40 per cent on average,7 which is slightly lower than the UK equivalent maximum combined uptake of 47 per cent.

The change in working habits has greatly reduced workers’ footfall in business and commercial districts in city centres, and the impact has been proportionally stronger in larger cities compared to smaller ones or towns.8 The change in central districts has also varied as, during periods of reduced restrictions, a significant number of office workers returned to their regular place of work – approximately one third of office workers in the UK compared to two thirds on average across Europe.9

Any long lasting post pandemic change to working patterns is likely to be more moderate than the change during the peak of the pandemic. It remains uncertain whether the opportunity for homeworking will continue for many UK employees, given that it has been made available under exceptional circumstances. However, almost one third of UK workers intend to work from home more often after the end of the pandemic than they did before.10

Socialising

Daily life in the UK during the pandemic has been drastically different compared to previously. Restrictions have led to steep reductions in social engagement levels, directly driven by stricter policy measures, such as hospitality closures. However, there has been no indication of a permanent reduction, as during times of eased restrictions, socialising levels partially recovered.11 Such changes in behaviour have also been observed globally in countries that followed similar policy approaches to reduce the rate of infection.12 Despite that, a long term reduction in socialising cannot be ruled out, as there was already a downwards trend in the frequency of socialising in recent years.13 14 Additionally, there are already indications of a heightened wariness of crowded places in particular, as a significant number of people intend to avoid them in the future more than they did before the pandemic.15

Housing

The pandemic has indicated that changing working and socialising habits can lead to changes in people’s motivations for housing choices. Demand for rural housing has significantly increased,16 and there has been an overall surge in the stated interest of city dwellers, such as Londoners, to leave the urban core in search of more space and better access to parks.17 However, there is no strong evidence yet of significant population movement. Recent trends indicate a convergence of rural and urban house price growth in 2020, with growth in rural house prices having been lower for most of 2019.18 However, this is not unprecedented as rural areas had considerably higher price growth than urban areas in 2018, which indicates that the long term trend may still be uncertain.

Transport

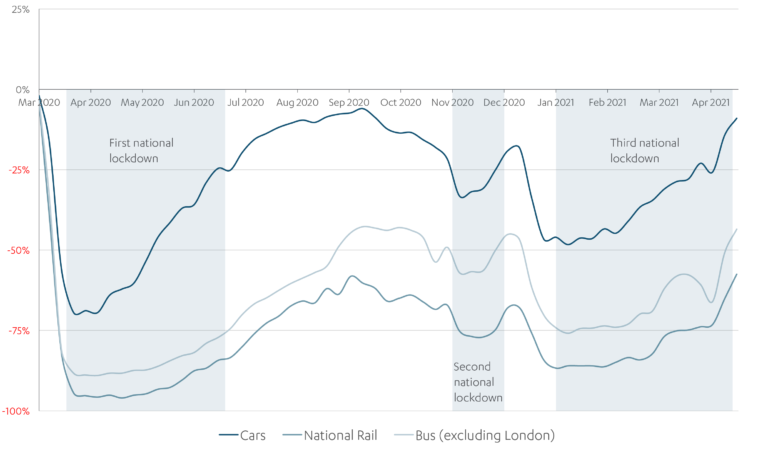

Use of different modes of public transport in the UK dropped approximately 80 to 95 per cent following the announcement of the initial March lockdown,19 which has also been the case globally where there have been severe mobility restrictions.20 Even during times of reduced restrictions, overall public transport use has not fully recovered.21

The impact on different modes of transport has not been equal. The decrease in rates of use of Transport for London Tube and National Rail has been significantly greater than for buses.22 At the highest point of transport use in the pandemic, in September 2020, National Rail reached 42 per cent of its normal use compared to around 58 per cent for buses. This is possibly due to the prevalence of homeworking, as city centres’ office workers use the Tube and National Rail proportionally more than bus services. This indicates that changing working habits could impact different modes of transport in different ways.

Motor vehicle use reduced less steeply than public transport, but the impact was still significant, decreasing by up to 70 per cent. However, it has also recovered much faster and, in the case of commercial vehicles, even surpassed previous levels of use23 – a few months after the initial lockdown, there was an increase in commercial vehicles usage of ten to 20 per cent in some weeks. This can possibly be attributed to increased online shopping activity, which almost doubled during the pandemic.24 Car use has also recovered almost fully during months of reduced restrictions, but there has been no evidence of increased car ownership,25 which could indicate that people are not yet making decisions about long term preferences.

Mobility restrictions have also prompted a surge in active travelling. Following the initial lockdown, cycling rates increased by approximately 50 to 100 per cent during most weeks of April and May 2020.26 In the following months cycling uptake remained at slightly higher levels compared to pre pandemic, albeit lower compared to the initial surge. This suggests that the increased uptake observed may have been a short term impact.

Transport use mainly depends on people’s working and socialising habits, as well as their home locations. The pandemic has established that a surge in homeworking and avoidance of socialising directly results in significant decreases in transport use, especially in public transport.

Figure 1.1: Transport use compared to an equivalent day in 2019 between March 2020 and April 2021 in Great Britain (weekly average)272829

Note: shaded lockdown areas based on the first date lockdowns were imposed to the first easing of restrictions. These capture the period of highest restrictions.

Digital

Homeworking and mobility restrictions have led to a significant increase in the time spent online,30 which peaked in April 2020. However, increases in data demand for fixed networks were mostly concentrated throughout the day rather than during the evening peak hour. This has allowed digital communications networks to cope with demand as the impact has mostly affected demand distribution rather than peak demand.31 A similar pattern has occurred across Europe, as no operators reported significant network congestions.32 The pandemic has also significantly accelerated the adoption of digital services, such as online shopping and video conferencing.33 Overall data demand growth was already high in recent years,3435 but a further acceleration of this trend cannot be ruled out if an increased uptake of data-demanding services occurs.

Energy, waste and water

Changes in people’s living conditions during the pandemic have led to a partial transfer of utilities demand from workplaces, hospitality venues and shops to households. Overall demand for energy has reduced between 2019 and 2020 in the UK as well as globally, with peak reduction rates of more than ten per cent in some cases.36 Electricity demand has decreased significantly37 but domestic consumption has increased slightly overall, as people have been spending more time at home.38 In contrast, commercial consumption has declined significantly,39 and by up to 20 per cent in many sectors.40

Additionally, noticeable changes have been observed in the pattern of demand,41 as people’s daily lives adjusted to the new norm. However, the security of supply has not been compromised at any point.42 This indicates that a moderate long term behaviour change may not pose a challenge for electricity networks.

The increased number of people staying at home has also led to large increases in domestic waste.43 Equivalently, commercial waste has seen a large decline as,44 in practice, a significant share of the produced waste was being produced at home. Similarly, water demand previously generated by premises such as gyms and offices has been relocated to the home.45 The pandemic has established that changing working and socialising habits can affect spatial and temporal distribution of demand, but there has been no indication that current infrastructure was unable to cope.

Next Section: 2. Understanding behaviour change

The nature and extent of the shock caused by the Covid-19 pandemic has few recent precedents. This means that it is hard to predict the likelihood and nature of any long term behaviour change. The Commission has looked at academic theories of behaviour change and previous comparable shocks to help understand the potential for long term behaviour change following the pandemic.

2. Understanding behaviour change

The nature and extent of the shock caused by the Covid-19 pandemic has few recent precedents. This means that it is hard to predict the likelihood and nature of any long term behaviour change. The Commission has looked at academic theories of behaviour change and previous comparable shocks to help understand the potential for long term behaviour change following the pandemic.

Theories of behaviour change suggest there are certain factors that make long term behaviour change more likely. These include whether individuals have the capacity and opportunity to change behaviour, whether organisations facilitate or enable behaviour change, and whether people are motivated to change behaviour.

Analysis of comparable historic shocks suggests that permanent behaviour change is relatively unlikely, and few events have triggered long lasting behaviour change. However, behaviour change appears to be more likely when shocks are disruptive and prolonged which cause individuals or firms to find alternative behaviours, and when there is flexibility to change behaviour. This suggests that the Covid-19 pandemic may meet the conditions to trigger long term behaviour change.

The insights covered in this chapter have also been used to inform the development of scenarios for behaviour change used in the analysis in this report. For example, they have been used as a guide to the extent of changes that might occur in the scenarios used, reflecting that individuals generally need several factors in place to adopt and maintain new behaviours.

Theories of behaviour change

In the context of infrastructure demand, behaviour change includes changes in patterns of economic activity such as working and leisure, and changes in patterns of the use of infrastructure services by the public and businesses. There is existing academic research into what causes long term changes to these behavioural patterns.

Understanding this existing research and theoretical principles of what causes long term behaviour change can help identify plausible scenarios that may arise as a result of the Covid-19 pandemic. The Commission carried out a review of the literature, with the support of an expert panel, to explore the key models of behaviour change.

There are numerous models that predict behaviour change. Broadly, these models can be grouped into two categories, those with an individual focus and those with a more external and social focus.

Models with an individual focus primarily capture theories from psychology, where the individual is the key agent of change.46 These models suggest that behaviour change is more likely when:

- individuals have the capacity to carry out a behaviour and have a perception of control over that ability

- the wider environment can facilitate the behaviour and societal norms which consider the behaviour to be positive or expected

- there is personal motivation, conscious or otherwise, to carry out the behaviours.

For example, an individual’s decision to return to the office when restrictions allow may depend on the uptake of office working by others around them.

The COM-B model

One model that provides particularly useful insight into how behaviours develop and persist is the COM-B model, which has an individual focus and was designed to categorise behaviour change interventions. The model identifies three factors required for behaviour change to occur: capability, opportunity and motivation.47

The greater the capability and opportunity, the more likely motivation is to be present and thus, the more likely a behaviour is to occur. The COM-B model offers a useful framework to assess whether behavioural trends are likely to continue and similarly, whether alternative behaviours are likely to emerge.

Models with an external focus often assume individuals exist in and are influenced by a social environment.48 These models show that:

- perceived consequences can impact behaviour change

- actual consequences can reinforce a behaviour directly or indirectly through the wider environment.

For example, an individual’s behaviour may be affected by the perceived health risk of Covid-19.

Using the conclusions from the theories of behaviour change, particularly the COM-B model, the Commission has developed the following framework for assessing the likelihood of long term behaviour change:

- do individuals or the relevant populations have the physical capacity to enact the behaviour and is this likely to increase or decrease?

- do individuals or the relevant populations have sufficient understanding, knowledge or memory to carry out the behaviour and is this likely to increase or decrease?

- is there likely to be sufficient physical environmental opportunity for the behaviour to occur?

- what are the social norms and how are they likely to develop?

- will organisations be likely to facilitate the behaviour?

- are there any instinctive or habitual drivers likely to impact the behaviour?

It is possible to apply this framework to the Covid-19 pandemic as follows:

- some individuals have had the capacity and opportunity to use technology to work from home, but this may decrease if workers are required to return to the office at least some of the time

- some individuals and organisations are likely to have spent time and money on skills and equipment to support the shift to remote working, which combined with the reduced costs of avoiding a commute to work, may drive motivation for individuals to continue working from home in the future

- the environmental opportunity for behaviour change to occur will depend on organisations’ approach to workers’ return to offices – the UK has a high proportion of desk based work, which may mean there is more environmental opportunity for employers to save property costs by encouraging employees to work remotely

- it is difficult to determine how social norms will evolve following the pandemic as people typically do not make behavioural choices in isolation but respond dynamically to what others do

- aversion to the risk of infection may leave a permanent distaste for crowds and in-person socialising, however it may equally have underlined the importance of face to face interactions – and this may vary between social groups.

Applying the framework shows that there is potential for long term behaviour change following the pandemic. However, the nature and extent of the change remains unpredictable as the situation continues to evolve, and any long term behaviour change is likely to rely on several complementary factors being in place. These insights have been used to help develop scenarios of behaviour change used in the analysis in this report.

Analysis of historic shocks to infrastructure demand

The nature and extent of the shock caused by the Covid-19 pandemic has few recent precedents. However, assessing similar historical events can help to develop an understanding of:

- the effect of historic shocks on infrastructure demand

- the characteristics of and policy responses to historic events that triggered long term behaviour change

- the factors that caused behaviour change to be permanent or temporary.

As part of this project, a comparative analysis of a range of historical events that affected infrastructure demand was undertaken for the Commission.49 The historic examples used for the analysis were disruptive events which impacted a system to such a degree that operational management of the system was required to mitigate harmful impacts. Case studies were selected on this basis to ensure that they shared characteristics of the Covid-19 pandemic. The events included shocks such as the Oil Crisis in 1973 and the Auckland Blackout in 1998.

The analysis suggests that permanent behaviour change is less likely to emerge than might be expected. Firstly, few substantial events have triggered long lasting behaviour change. A key example of this is the 9/11 terrorist attack. Whilst there was a temporary reduction in public transport usage due to fear of another attack, ridership levels recovered shortly after the event. Long term impacts on behaviour change were constrained as the perceived risk of future attacks did not persist after the initial one.

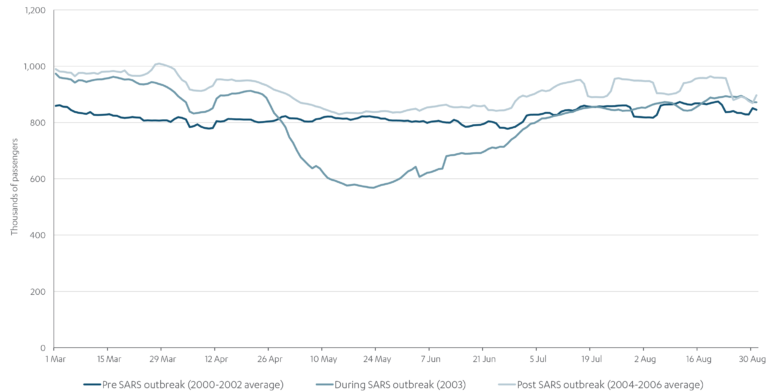

The principles of the COM-B model can also help understand why shocks did not trigger long term change and why future shocks may not either. For example, the SARS outbreak in 2003 caused a temporary fall in public transport usage due to the risk of contagion. However, this was a short term change and ridership returned to previous levels due to the absence of an alternative method to travel to work. Figure 2.1 illustrates that the fall in the Taipei Underground usage was only temporary, with ridership levels recovering soon after.

Figure 2.1 – Comparison of Taipei Underground patronage in March to August before, during and after the SARS outbreak, rolling 7-day average50

The COM-B model suggests that there was not sufficient capability or opportunity to commute to work and avoid public transport – car ownership is low in Taiwan, constraining both capability and opportunity. The SARS outbreak did, however, establish the regular habit of wearing masks on public transport for many riders.

The key conclusions from the comparative analysis were that:

- disruptive and prolonged shocks are generally more likely to cause long term changes in behaviour, as shocks of this nature force individuals and firms to find alternative practices or services to meet their needs

- the perceived risk to health or safety has tended to fall over time in the absence of further events to reinforce it

- new practices are more likely to develop when individuals and firms have sufficient flexibility to change their behaviour

- policy mechanisms can affect the likelihood of long term behaviour change by either increasing or decreasing the flexibility to use alternative practices, which in turn will either mitigate or reinforce the impacts of shocks.

Studying the current situation through this lens may suggest that the conditions for long term behavioural change due to Covid-19 are present. During the pandemic, a significant portion of the workforce has had the ability to work from home. This flexibility to adapt and respond to disruptive pressures was not present during other disruptive events in the past, such as Hurricane Sandy or the Auckland Blackout. At the time of these events, long term remote working was not feasible, as internet and business systems did not allow for productive working from home. As a result, remote working was only a temporary change and employees soon returned to the office. Following the pandemic, while uncertainty remains, it is possible that there will be a permanent shift in motivations combined with an ability to work from home, which could enable and cause long term behaviour change.

In summary, while there are only limited historical comparators, it is possible to combine lessons from past experiences with theories of behaviour change to gain a more nuanced understanding of the potential impacts of shocks to infrastructure demand. The Commission has used this to assess the likelihood of long term behaviour change, and to inform the development of scenarios of behaviour change set out in the next chapter.

Next Section: 3. Scenario analysis

The Commission has developed a set of scenarios reflecting different combinations of underlying behavioural trends that could affect future infrastructure use. The analysis shows that the range of possible outcomes is wide, and the impacts are likely to be greater in magnitude for transport than for the digital, energy, water and waste sectors. Changes in patterns of demand may have significant implications, even if changes to total demand are modest.

3. Scenario analysis

The Commission has developed a set of scenarios reflecting different combinations of underlying behavioural trends that could affect future infrastructure use. The analysis shows that the range of possible outcomes is wide, and the impacts are likely to be greater in magnitude for transport than for the digital, energy, water and waste sectors. Changes in patterns of demand may have significant implications, even if changes to total demand are modest.

This section sets out the Commission’s scenario based approach, summary of the analysis and key insights. The Commission used five different scenarios of possible behaviour change following Covid-19 to assess the impacts on infrastructure demand.

The Commission found that:

- the potential impacts of behaviour change on infrastructure demand are likely to be less significant than changes from other trends over the past thirty years, such as the number of passenger journeys by rail doubling

- there are a range of impacts across infrastructure sectors, and the spread of potential outcomes for transport is wider than digital and utilities sectors

- higher uptake of homeworking affects both public and private transport, but has the greatest impact on public transport

- permanent uptake of homeworking could make a difference to where people live and work

- there are different impacts on different places from changes to total demand and its distribution.

Full details of this analysis can be found in the technical annexes of this report.

Overall approach

A scenario based approach

Given the inherent uncertainty, the Commission has taken a scenario based approach to understanding the impacts of behaviour change on long term infrastructure demand following the Covid-19 pandemic. This is consistent with the Commission’s first National Infrastructure Assessment, which took a scenario based approach to understanding the impact of key ‘drivers’ (population, economic growth, technology, environment and climate change) on future infrastructure supply and demand.51

A scenario based approach to analysis of future infrastructure demand means policy and decision makers can prepare for a range of possible futures until it is clearer how things will settle. Taking strategy or financial decisions can be hard in an environment of uncertainty. Not deciding or postponing decisions – either to do more analysis or to wait until there is more certainty – is still a decision.52

Scenarios are a set of possible outcomes, including a narrative of how and why such outcomes would occur. The use of a scenario approach is useful when uncertainties cannot be properly described with quantitative probability distributions. But they will not eliminate uncertainty. Scenarios instead help to map out, analyse and sometimes quantify very specific uncertainties that are important to help make decisions. They can clarify how possible outcomes would affect the criteria for making those decisions.53

Core principles

The Commission has adopted the following principles in developing scenarios of behaviour change. The scenarios should:

- cover a plausible range of outcomes – they should not seek to cover the full range of possible futures however unlikely, nor have too narrow a focus of predicted futures given the level of uncertainty

- be based on a range of different behavioural responses, as set out in chapter two, to help understand how behaviour and behaviour change can drive changes in infrastructure demand

- should form coherent packages of futures, based on underlying interactions between behavioural trends, with each scenario forming a coherent picture of a plausible future across all activity, considering both the direct and indirect interactions between behavioural patterns.

Methodology summary

The Commission’s analysis considers five scenarios, providing a reasonable spread of possible outcomes and tests different combinations of behaviour responses. The scenarios are driven by different combinations and intensities of ‘underlying trends’, which demonstrate the bigger picture of what happens in each scenario and why. These underlying trends are highly relevant to infrastructure demand, necessarily focusing on the impact on urban centres, transport and digital connectivity. However, these trends do not reflect the full scope of possible behaviour change.

These trends are defined as follows:

- working from home: inclination of people and businesses (i.e. employers and employees) to adopt flexible working and/or homeworking

- social wariness: people being more cautious to participate in gatherings which involve being in close proximity to others

- dispersal from cities: inclination of people and businesses to locate in less densely populated areas, the opposite of the long term trend towards urbanisation and densification

- use of virtual tools: potential uptake of online and virtual activities in social, leisure, education, shopping and other activities.

These underlying trends interact: higher uptake of virtual tools is influenced and limited by the extent of social wariness and flexible working or homeworking, and dispersal from cities is more likely when rates of working from home and social wariness are higher. These interactions limit the number of plausible scenarios.

The five scenarios are defined qualitatively, including an overarching narrative and descriptions for each underlying trend. The impacts on infrastructure demand are then expressed qualitatively and quantitatively for the following broad sector groups:

- land use – impacts on location and patterns of economic activity, predominately where people live, work and do leisure activities

- transport – changes to number and types of journeys made on public and private transport, particularly across different times of the day, modes and purposes

- digital – impact on broadband demand for residential and commercial premises

- utilities – groups together impacts on energy, water and waste consumption for residential and commercial premises.

The analysis makes additional assumptions on the extent of the behaviour change expected in all five scenarios. These set a reasonable boundary for what might occur in all our scenarios, which is less than the maximum conceivable impact. These are:

- the number of people who are fully able to realise and maintain behaviour change is a sub-group of those who are potentially able to. This reflects the lessons in the previous chapter, which indicate that individuals generally need several factors in place to adopt and sustain new behaviours. The number of people who can potentially achieve behaviour change is also a fraction of the general population. For example, quantitative analysis undertaken for the Commission’s identifies that around 57 per cent of the working population work in occupations where there is potential to work from home.54

- population mobility is not unlimited. The analysis assumes that economic forces will limit locational choices of household and businesses in the future. Key limitations are adjustments to property prices. For example, higher demand to move to suburban and rural areas would push up demand and prices of property, but the opposite would also be true of more urban areas.

Summary of scenario analysis

This section sets out a summary of the key insights, bringing together the results from the qualitative and quantitative analysis. Table 2 sets out the five scenarios. Table 3 presents a summary of the impacts by broad sector grouping – transport and land use, and digital and utilities. Figures 3.1 to 3.7 present key results from the quantitative analysis undertaken for the Commission, demonstrating the spread of outcomes across scenarios and infrastructure sectors.55

Interpreting the results

The main insight from the analysis is the degree of variation between scenarios, not the total levels of demand projected. This is because long term infrastructure demand is driven by a range of factors such as economic and population growth, as well as changes in technology and the environment.56 This means a range of demand outcomes are possible depending on the sector – it could be higher, lower or broadly similar in 30 years’ time compared to today. This is demonstrated by recent trends in the past 30 years. For example, the number of passenger journeys by rail have more than doubled,57 while energy consumption has been broadly stable.58

However, the impact of behaviour change is likely to cause differences in the growth and level of demand over such time horizons. Depending on the infrastructure sector and scenario, future infrastructure demand may be higher or lower than otherwise expected as a result of behaviour change due to Covid-19.

Understanding the quantified impacts

The estimated quantified impacts are designed to test the sensitivity of infrastructure sectors to different scenarios of behaviour change due to Covid-19. These are based on simplified assumptions which capture ‘first round’ effects of behaviour change. It does not include second and third round effects, or feedback loops and tipping points that may arise following initial behaviour change. It also assumes there is no policy change that may incentivise certain behaviours or have wider macroeconomic implications that may affect infrastructure demand.

On that basis, total infrastructure demand is estimated for the period 2020 to 2055 in five yearly intervals for the sole purpose of scenario analysis. That enables a comparison of infrastructure demand outcomes across scenarios to assess the impact of behaviour change, given all other variables held constant (e.g. economic and population growth, policy change).

Because of the simplified nature of the analysis, the estimates should not be treated as a forecast of the future pathway of total infrastructure demand. This means it is difficult to make meaningful comparisons of infrastructure demand between 2020 and 2055. This is because several uncertain factors will drive demand and it is unknowable at this stage how important behaviour change will be compared to other drivers.

For example, some scenarios show higher rail demand in 2055 compared to 2020, while some show lower. However, to believe lower rail demand is possible in reality assumes that behaviour change is not only high and persistent, but dominates all other trends that drive demand (e.g. population and economic growth, resilience of cities, and future policy change that may incentivise certain behaviours).

A full demand modelling exercise would be required to forecast the pathway of infrastructure demand and deepen the Commission’s understanding of the potential impacts of behaviour change.

For the purposes of the Commission’s analysis, scenario 1 – where there is a reversion to pre pandemic norms – is used as the comparator for scenarios 2-5 based on the outcome in 2055 for transport and utilities sectors, and 2025 for digital.59 This applies to the quantitative and qualitative impacts reported in Table 3 and Figures 3.1 to 3.7.

Table 2: Scenario analysis – description of scenarios and intensity of underlying trends

| Scenario name | Working from home | Social wariness | Dispersal from cities | Use of virtual tools |

|---|---|---|---|---|

| 1) Reversion and reaction (comparator scenario) | Low. Very limited increases in flexible working | Low. Behaviours developed during the pandemic are not maintained | Low. Cities and other hubs are still important places for work, leisure and socialising | Low. Very limited change in existing trends such as increases in online shopping |

| 2) A more flexible future | Medium. Flexible working is adopted by employers and employees where it is practical and feasible to do so | Low. Behaviours developed during the pandemic are not maintained | High. Cities continue to be key areas for living, although there is higher demand to live in more suburban areas | Medium. Existing trends accelerate – increase in virtual activities in shopping and other domains |

| 3) Low social contact urban living | Low. Very limited increases in flexible working | High. Behaviours developed during the pandemic are maintained. People generally socialise less | Low. Cities and other hubs continue to be key areas for living, particularly living close to workplaces | High. Existing trends accelerate significantly – increase in virtual activities in shopping and other domains |

| 4) Social cities | High. Homeworking is adopted at a high level by employers and employees where it is practical and feasible to do so | Low. Behaviours developed during the pandemic are not maintained | Low. Cities and other hubs are still important places for leisure and socialising | Medium. Existing trends accelerate – increase in virtual activities in shopping and other domains |

| 5) Virtual local reality | High. Homeworking is adopted at a high level by employers and employees where it is practical and feasible to do so | High. Behaviours developed during the pandemic are maintained. People generally socialise less | High. There is high demand to move to suburban and rural areas, or to other regions | High. Existing trends accelerate significantly – increase in virtual activities in shopping and other domains |

Note: full scenario descriptions can be found in the methodology annex.

Table 3: Scenario analysis – summary of impacts by sector

| Scenario name | Land use & transport | Digital & utilities |

|---|---|---|

| 1) Reversion and reaction (comparator scenario) | • Extremely limited changes in patterns of economy activity • Urban centres still important for living and working, and other activities such as leisure and socialising • Public and private transport use return to pre-pandemic trends | • Demand growth in digital communications continues to follow a similar long term trajectory as before • Consumption trends of energy, water and waste remain similarly unchanged, with similar shares between residential and commercial premises. |

| 2) A more flexible future | Compared to scenario 1 there is: • a very similar pattern of economic activity due to continued importance of urban centres for working and socialising • higher demand from households to live further away from their workplace in more suburban or rural areas, although actual population movements are extremely limited • up to ten per cent lower trips by public transport due to less commuting and business travel (i.e. more meetings and workplace events done virtually), which could result in a flattening of peak demand during the working day and week • no change in the use of public transport and aviation for leisure and tourism • higher growth in online shopping which increases demand for deliveries to households, increasing the share of ecommerce in freight activity. | Compared to scenario 1 there is: • less than ten per cent increase in digital demand • broadly similar consumption of energy, waste and water • a shift in the share of digital and utilities consumption towards residential premises away from commercial due to flexible working and increased adoption of digital services. |

| 3) Low social contact urban living | Compared to scenario 1 there is: • a very similar pattern of economic activity due to continued importance of urban centres of working, despite decline in use of retail, hospitality, and other facilities • 20 per cent lower trips by public transport due to less travel for leisure and other activities, and to some extent commuting from limited increases in flexible working • lower use of aviation for leisure, tourism and other activities • a shift from public towards private (e.g. car) and active (e.g. walking, cycling) transport modes for commuting, social and leisure activities • higher growth in online shopping which increases demand for deliveries to households, increasing the share of ecommerce in freight activity. | Compared to scenario 1 there is: • a ten per cent increase in digital demand due to a very increased adoption of digital services • broadly similar consumption of energy, waste and water • a shift in the share of digital and utilities consumption towards residential premises away from commercial due to flexible working and increased adoption of digital services, and more time spent at home and less time using retail, hospitality, and other facilities. |

| 4) Social Cities | Compared to scenario 1 there is: • a very similar pattern of economic activity despite increase in homeworking, urban centres and other hubs still important for leisure and social activities • up to 15 per cent lower trips by public transport due to less commuting and business travel, which may result in a flattening of peak demand during the working day and week • no change in the use of public transport and aviation for leisure and tourism • higher growth in online shopping which increases demand for deliveries to households, increasing the share of ecommerce in freight activity. | Compared to scenario 1 there is: • less than ten per cent increase in digital demand due to homeworking and increased adoption of digital services • a slight increase in the consumption of energy, waste and water • a shift in the share of digital and utilities consumption towards residential premises away from commercial due to homeworking and increased adoption of digital services. |

| 5) Virtual local reality | Compared to scenario 1 there is: • higher demand from households to live further away from their workplace in more suburban or rural areas, and other city regions • potential changes in patterns of economic activity with a relative decline in urban centres and other hubs for living and working, and other activities such as leisure, socialising and shopping • local amenities near to where people live may grow in importance • 25 per cent lower trips by public transport due to less commuting and business travel, which may result in a flattening of peak demand during the working day and week • lower use of public transport and aviation for leisure, tourism, shopping and other activities declines significantly • a shift from public towards private (e.g. car) and active (e.g. walking, cycling) transport modes for a range of purposes • higher growth in online shopping which increases demand for deliveries to households, increasing the share of ecommerce in freight activity. | Compared to scenario 1 there is: • a ten to 15 per cent increase in digital demand due to homeworking and very increased adoption of digital services • less than 10 per cent increase in the consumption of energy, waste and water • a shift in the share of digital and utilities consumption towards residential premises away from commercial due to homeworking and increased adoption of digital services, and more time spent at home and less time using retail, hospitality, and other facilities. |

Key transport sector results from quantitative analysis

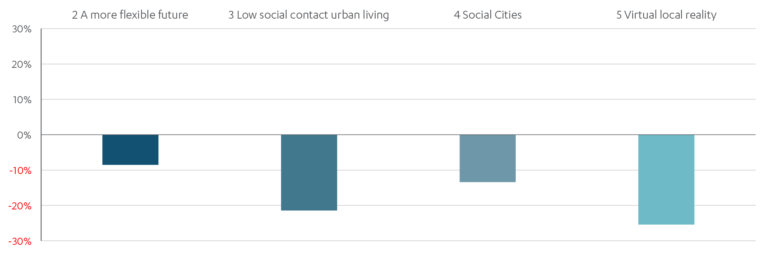

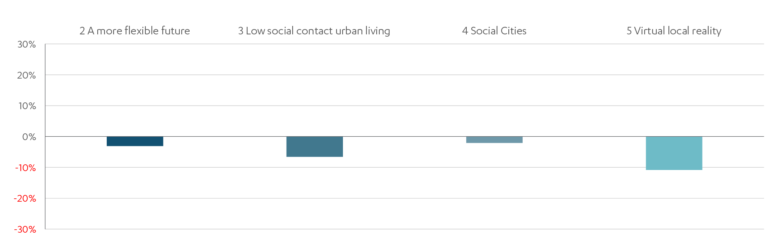

Figure 3.1 Comparison of total annual trip rates for public transport in 2055 in England (percentage difference in scenarios 2-5 compared to scenario 1)

Note: public transport includes bus, surface rail and other public transport modes

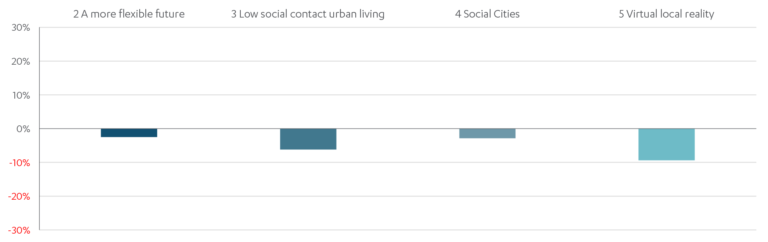

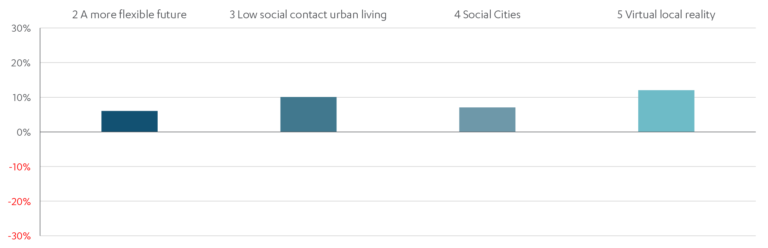

Figure 3.2: Comparison of total annual trip rates for private transport in 2055 in England (percentage difference in scenarios 2-5 compared to scenario 1)

Note: Private transport includes car and other private transport modes

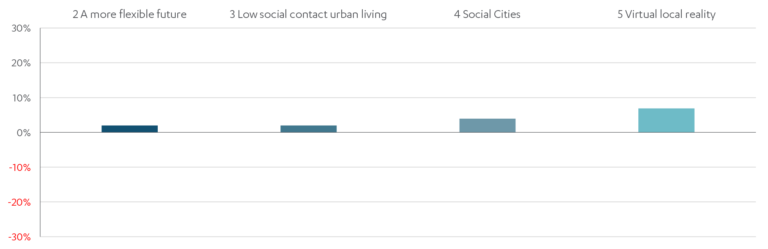

Figure 3.3: Comparison of total annual trip rates for active modes in 2055 in England (percentage difference in scenarios 2-5 compared to scenario 1)

Note: active modes includes cycling and walking

Key digital, water, waste and energy sector results from quantitative analysis

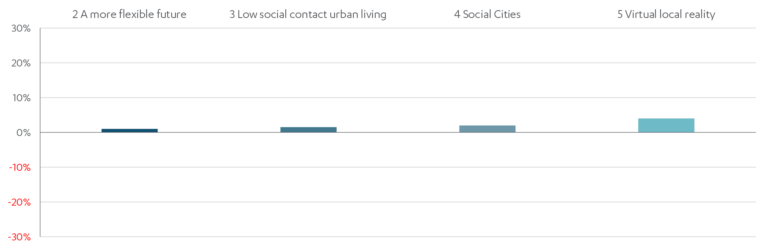

Figure 3.4: Comparison of domestic monthly data demand (petabytes) in 2025 in the UK (percentage difference in scenarios 2-5 compared to scenario 1)

Figure 3.5: Comparison of domestic water consumption per day (megalitres) in 2055 in the UK (percentage difference in scenarios 2-5 compared to scenario 1)

Figure 3.6: Comparison of domestic waste generated per year (thousands of tonnes) in 2055 in the UK (percentage difference in scenarios 2-5 compared to scenario 1)

Figure 3.7: Comparison of energy consumption per year (gigawatt hours) in 2055 in the UK (percentage difference in scenarios 2-5 compared to scenario 1)

Key insights

The potential impacts of behaviour change on infrastructure demand are likely to be less significant than changes from other trends over the past thirty years.

Recent trends in infrastructure demand show that a range of change is possible. In the past 30 years, the number of passenger journeys by rail have more than doubled,60 while energy consumption has been broadly stable.61

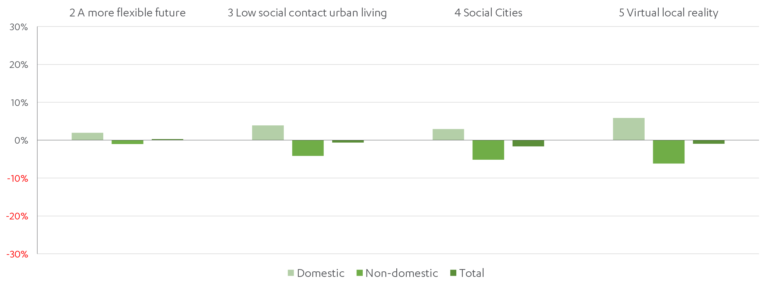

By comparison, the spread of outcomes for future public transport is 25 per cent between the lowest (scenario 1) and highest (scenario 5) behaviour change scenario. This is a considerably smaller change compared to recent trends. Impacts on total energy consumption across all scenarios are modest at best, broadly in line with recent trends. However, the main implication for energy and other utilities is a potential shift towards domestic consumption away from non-domestic due to reduced use in workplaces, leisure and hospitality buildings.

There are a range of impacts across infrastructure sectors, but the nature of public transport means that spread of potential outcomes is wider than digital and utilities sectors.

The impact on public transport can be significantly affected by relatively small changes to working and socialising patterns, and public preferences between different modes of transport, which will not affect the digital and utilities sectors to quite the same extent.

Public transport is disproportionally impacted because the size and physical nature of the network, as well as user pricing (i.e. fares), are geared towards peak rather than average demand. For example, rail travel in major UK cities is dominated by peak travel, with commuting for work and education being the most common journey purpose for passengers.62 A reduction in average demand while peak demand stays the same, or a reduction in peak demand while there is still demand for regular services, would require public transport networks to deliver similar levels of service with less income from fares.

Public transport is mainly affected by changes in working patterns, but also combinations of all underlying trends either working together (e.g. scenario 5) or in opposition (e.g. scenarios 3 and 4). Avoidance of crowding may reduce use of public transport, and transport demand generally may be relatively lower if people socialise less and do more activities online – whether people work more from home or not.

In addition, in public transport there is also competition between different modes. This is both within public transport (e.g. rail, bus) and between private (e.g. car) and active modes (e.g. walking and cycling). The number and type of journeys taken are affected by a range of factors including individual preferences, the price of different modes, and where people live and work.

Like transport, digital and utility networks are similarly physically structured for peak demand. However, the main difference is that these sectors are priced at average demand and competition within sectors is radically different. In the case of energy and water, switching supplier doesn’t change the final product consumed, even if the consumer saves money from a lower bill. This applies to an extent with digital, but there is greater product differentiation because the availability and quality of broadband received scales with price and varies by geographic location (e.g. urban and rural).

What this means is that digital and utilities sectors are less sensitive to behaviour change due to pandemic compared to public transport. In addition, while the analysis shows the size of the impacts are likely to be modest, these are unlikely to have significant consequences. As outlined in chapter one, digital capacity is likely to keep pace with change in working patterns and increasing uptake of virtual activities. Utility networks also coped well during periods of high restrictions during the pandemic, with higher domestic consumption offset by lower consumption in non-domestic buildings.

Higher uptake of homeworking affects both public and private transport but has the greatest impact on public transport.

Less commuting and travel for other purposes has a larger impact on public than private transport with certain occupations that are likely to work from home also likely to commute by public transport such as rail. However, because most commuters overall use the car, higher homeworking may result in up to 10 percent lower car use compared to scenario 1.

Permanent uptake of homeworking could make a difference to where people live and work.

More flexible working or homeworking could see households moving from urban centres to suburban and rural areas, or between regions – potentially significantly if urban living is valued less both for work and socialising.

However even if people wish to leave the cities, ability to change location may turn out to be constrained in practice. Some occupations are more likely to have the motivation and opportunity to adopt flexible working and homeworking than others. Without significant rural or suburban housebuilding the availability of homes will limit the number of households that can move.

In other words, there are practical limits to how much change is likely, and it is equally plausible that change may be more limited. Constraints to change may be higher in the short term, whereas in the long term policy change may reduce this (e.g. more housebuilding allowed in rural areas to meet permanently higher demand).

There are different impacts on different places from changes to total demand and its distribution.

Cities are particularly impacted by changes in homeworking and socialising, with knock-on effects to urban transport networks. These networks underpin commuter journeys, creating deep labour markets and enabling people to access cultural and leisure activities.63

Therefore, less commuting and travel for other purposes such as leisure and shopping is likely to lead to lower than anticipated total demand for public transport. Depending on the scenario, this may flatten peak demand during the working day and week or create a new peak (e.g. if employees who work flexibly generally go into the workplace on a particular day).

However, other types of places (e.g. suburbs, towns, rural areas) may be affected for different reasons, and localised effects are possible. For example, population movements to these areas may place additional pressure on existing networks, particularly roads (where there is less public transport). Rural residents for example tend to make more and longer journeys by car compared to more urban residents.

Next Section: Conclusions and next steps

Significant uncertainty still exists around the continuation of the behaviour changes observed during the Covid-19 pandemic and their effects on infrastructure demand. However, the Commission’s analysis shows that modest changes in behaviour can lead to changes in overall demand or its distributional patterns, with particularly strong impacts for public transport, raising questions about how to plan for the future.

Conclusions and next steps

Significant uncertainty still exists around the continuation of the behaviour changes observed during the Covid-19 pandemic and their effects on infrastructure demand. However, the Commission’s analysis shows that modest changes in behaviour can lead to changes in overall demand or its distributional patterns, with particularly strong impacts for public transport, raising questions about how to plan for the future.

The challenge of planning for the future can be addressed by a combination of data driven decision making, applying low regrets strategies, and using an adaptive approach to infrastructure planning.

Uncertainty

People’s behaviour can be affected by environmental factors, however, it cannot be assumed that it will follow a specific trajectory. Historic shocks have shown that changes to behaviour tend to be significantly stronger in the short term, even if they may evolve into long term shifts.

We have observed significant shifts in behaviour during the Covid-19 pandemic, particularly during its peak. Phenomena such as the uptake of homeworking, avoidance of public transport and adoption of digital services led to a new way of living for a significant part of the UK population. In some cases, behaviour has fluctuated during the pandemic, showing signs of recovery at times of reduced restrictions. However, there have been impacts that have persisted to a significant degree for a full year or more.

There is uncertainty as to how many of these changes to behaviour will continue in the coming years. There is as yet no clear pattern of what will unfold around behaviours such as working from home, socialising, housing preferences, or using digital services.

Behaviour change can impact infrastructure

It is still too early to draw conclusions about what behavioural preferences may emerge in the long term, however, a few key lessons are available now. The Commission’s analysis shows that relatively modest changes in behavioural patterns may have big implications for infrastructure demand, especially for public transport use.

Changes in the distribution of demand can be as significant as changes in its total level particularly for networks that are built to manage peak time capacity. Flexible working may mean flatter peaks on public transport, potentially reducing the level of capacity required.

Additionally, modest changes in demand may also have disproportionate effects where crucial tipping points are reached. For example, a small amount of additional road traffic could lead to congestion in some town centres, potentially slowing journey times considerably. For some public transport services, a small reduction in passengers could lead to a downward spiral in revenues, possibly leading some services to be discontinued.

Even in scenarios where preferences change radically, the potential for change in infrastructure use is not unlimited. Some economic sectors and social activities have not changed much even during the period of restrictions, and locational preferences will be constrained by the availability of property.

Some sectors will clearly be more affected than others. Transport, and particularly public transport, may potentially see significant changes in use levels and distribution of demand, even for relatively modest changes in preferences around working and socialising patterns.

Planning for an uncertain future

It is still far too early to draw conclusions about which behavioural trends may emerge in the long term as a result of the pandemic. In the UK, offices have not yet fully reopened. New arrangements are being proposed by several employers, but these are still to be tested. Social habits will not follow organisationally chosen pathways and may change direction some time after restrictions are eased.

However, the importance of a continued commitment to infrastructure remains high given its critical role in supporting policy goals such as net zero greenhouse gas emissions by 2050 and rebalancing economic growth across the UK. Although uncertainty may point towards delaying decisions on major infrastructure projects, there is also a case for the government to take decisions to reduce uncertainty and increase confidence for the market and for investors.

Alongside the role of infrastructure investment in supporting the economic recovery, the government should maintain focus on future infrastructure needs to achieve long term goals. To inform upcoming decisions on infrastructure and remain responsive to a breadth of outcomes, policymakers should consider the following questions:

- What decisions are unaffected by uncertainty in behavioural patterns? Whilst outcomes for different sectors will vary depending on which scenario plays out, there are some areas which are likely to be less affected by the Covid-19 pandemic. For example, it is certain that in any scenario for behaviour change, decarbonisation of infrastructure will remain necessary to achieve net zero by 2050.

- When will it be clear which behaviours will be permanent? Better data gathering on indicators of how behaviour change may be manifesting, with attention to ensuring this data is timely, can help identify emerging behaviour change promptly. Additionally, it is important to avoid reliance on models that have not worked that well even under more stable conditions in the past.

- Should policy seek to influence which scenario unfolds? The outcomes of some scenarios are likely to be less preferable than others, with varying combinations of positive and negative consequences. Policymakers should consider how policy can encourage preferred shifts in behaviour. For example, as people’s patterns of transport use are changing in response to the pandemic, there is scope to encourage more active travel or avoid a recovery scenario in which travel by car rises relative to pre-pandemic usage. Transport providers can also consider how best to ensure consistent, evidence-based information is provided to give passengers confidence to use public transport.

- How can long term project commitments be reconciled with ongoing uncertainty? The portfolio of infrastructure investments can mitigate uncertainty by adopting a balance across different levels of risk, and having a complementary mix of programmes which cover different scenarios as well as low regrets options applicable across multiple scenarios. A particularly valuable tool may be the adaptive approach to rail investment, as considered by the Commission in the Rail Needs Assessment for the North and Midlands (RNA).64 The RNA proposed rail investment moving forward in stages as costs and benefits become clearer. An adaptive approach would allow for measured, forward momentum that can be modified as the long term behaviour changes become evident. In turn, this can help to preserve optionality and flexibility throughout a project. This will be particularly important in sectors where there is greater uncertainty, such as transport.

These considerations will guide the Commission in its future work, including making policy recommendations in the study underway on Infrastructure, Towns and Regeneration, and in the second National Infrastructure Assessment.

Next Section: Acknowledgements

The Commission is grateful to everyone who engaged with the development of this report. The list below sets out organisations that have engaged with the Commission in delivering this paper.

Acknowledgements

The Commission is grateful to everyone who engaged with the development of this report. The list below sets out organisations that have engaged with the Commission in delivering this paper.

The Commission would also like to acknowledge the contribution its expert advisory group has made to this paper, and would like to thank Nida Broughton, Andreas Cebulla, Brian Collins, Nigel Gilbert, Natasha McCarthy and Ine Steenmans for their support.

The Commission is grateful to officials from across government and other individuals who have engaged with the assessment.

The Commission would like to acknowledge the members of the Secretariat who worked on the report: Hannah Brown, Peter Burnill, Jen Coe, Nick Francis, James Heath, Catherine Jones, Kirin Mathias, Greg McClymont, Vasilis Papakonstantinou, James Richardson and Christopher Wanzala-Ryan.

Department for Transport

HM Treasury

Network Rail

Steer

Transport for London

University College London

References

- The paper does not aim to forecast future demand for infrastructure sectors, which will depend on many factors including economic and population growth, technology, behaviour change and policy choices. Rather the paper looks at the estimated impact of post pandemic behaviour change on future infrastructure demand under different scenarios.

- Felstead and Reuschke (2020), Homeworking in the UK: before and during the 2020 lockdown

- Felstead and Reuschke (2020), Homeworking in the UK: before and during the 2020 lockdown

- Office for National Statistics (2020), Coronavirus and homeworking in the UK

- Office for National Statistics(2021), Coronavirus and the social impacts on Great Britain

- Office for National Statistics(2020), Coronavirus and homeworking in the UK

- European Commission (2020), Telework in the EU before and after the COVID-19

- Centre for Cities (2020), High Street Recovery Tracker

- The Guardian (2020), UK office workers slower to return to their desk after Covid

- Office for National Statistics (2020), Changes in behaviours during and after the Coronavirus pandemic

- Office for National Statistics (2020), Coronavirus and the social impacts on Great Britain

- University of Oxford (2020), Coronavirus Government Response Tracker

- Office for National Statistics (2020), Social capital headline indicators

- Department for Transport (2019), National Travel Survey

- Office for National Statistics (2020), Changes in behaviours during and after the Coronavirus pandemic

- The Guardian (2020), UK country house prices hit four year high

- London Assembly (2020), Escaping the city post-covid

- Office for National Statistics (2021), Recent trends in the housing market

- Department for Transport (2021), Transport use during the coronavirus pandemic

- Google (2020), Mobility reports

- Department for Transport (2021), Transport use during the coronavirus pandemic

- Department for Transport(2021), Transport use during the coronavirus pandemic

- Department for Transport(2021), Transport use during the coronavirus pandemic

- Office for National Statistics (2021), Internet sales as a percentage of total retail sales

- Department for Transport(2020), Vehicle Licensing Statistics

- Department for Transport(2021), Transport use during the coronavirus pandemic

- Department for Transport (2021), Transport use during the coronavirus pandemic

- Institute for Government (2021), Timeline of UK coronavirus lockdowns, March 2020 to March 2021

- Cabinet Office (2021), COVID-19 Response – Spring 2021

- Ofcom (2020), Effects of Covid-19 on online consumption in the UK

- Ofcom (2020), Connected Nations 2020

- European Commission (2020), Digital solutions during the pandemic

- Ofcom (2021), Effects of Covid-19 on online consumption in the UK in 2020

- Ofcom (2015), Time spent online doubles in a decade

- Ofcom (2019), Online Nation

- Peng Jiang et al. (2021), Impacts of COVID-19 on energy demand and consumption

- Drax (2020), Electric Insights

- Shell (2020), How lockdown has impacted energy and broadband usage

- Department for Business, Energy & Industrial Strategy (2020), Energy trends

- UKERC (2020), COVID-19: The implications of the pandemic on the UK energy sector

- Deloitte (2020), The impact of COVID-19 on European power markets

- National Grid ESO (2020), Winter Outlook

- ADEPT (2020), Waste Survey Results

- ADEPT (2020), Waste Survey Results

- University of Manchester (2020), Coronavirus lockdown caused dramatic changes in water consumption

- Forest Research (2012) Theories: Behaviour Change

- West and Michie (2020), A brief introduction to the COM-B Model of behaviour and the PRIME theory of motivation

- Glanz et al. (2005) Theory at a Glance – A guide for Health Promotion Practice (Second Edition

- McArthur, Smeds and Zervaj (2021), The impacts of historic shocks on infrastructure demand

- Metro Taipei, Ridership counts.

- National Infrastructure Commission (2015), Congestion, Capacity, Carbon: priorities for national infrastructure- Modelling Annex

- International Transport Forum (2016), Strategic Infrastructure Planning: International Best Practice

- International Transport Forum (2016), Strategic Infrastructure Planning: International Best Practice

- Steer (2021), Infrastructure Demand Quantitative Analysis for Scenarios of Behaviour Change

- Steer (2021), Infrastructure Demand Quantitative Analysis for Scenarios of Behaviour Change

- National Infrastructure Commission (2017), National Infrastructure Assessment. Please see ‘expert research – general’ under supporting evidence for list of drivers papers on population, economic growth, technology, environment and climate change.

- National Infrastructure Commission, Historic Transport Dataset. Comparison of the total number of passenger journeys by rail in Great Britain in 1990 and 2018.

- National Infrastructure Commission, Historic Energy Dataset. Comparison of total energy consumption by final user in the UK in 1990 and 2018.

- Steer (2021), Infrastructure Demand Quantitative Analysis for Scenarios of Behaviour Change. This report explains why digital demand is not projected beyond 2025.

- National Infrastructure Commission, Historic Transport Dataset. Comparison of the total number of passenger journeys by rail in Great Britain in 1990 and 2018.

- National Infrastructure Commission, Historic Energy Dataset. Comparison of total energy consumption by final user in the UK in 1990 and 2018.

- Department for Transport (2019), Rail Factsheet, December 2019.

- National Infrastructure Commission (2020), Rail Needs Assessment for the Midlands the North

- National Infrastructure Commission (2020), Rail Needs Assessment for the Midlands the North

Behaviour change and infrastructure beyond Covid-19

Commission analysis of a range of scenarios for how the use of public transport, broadband networks and utilities might change as a result of the pandemic.

Latest Updates

Coming up in 2024